What Your Client Is Actually Buying: The Science Behind a §45Q Carbon Tax Credit

Before you can advise on the tax treatment, you need to understand the underlying asset

Most CPAs are comfortable with the tax side of a §45Q transferable credit transaction. IRC §6418, Form 3800, the §38 general business credit ceiling — that's familiar territory. What's less familiar, for many advisors, is the physical asset that generates the credit in the first place.

That gap matters. If a client asks why this credit qualifies under §45Q, or what distinguishes a legitimate carbon sequestration credit from a poorly documented one, the answer lives in the science — not the statute. This article gives you the working vocabulary to have that conversation confidently.

The Statutory Starting Point

Section 45Q provides a federal income tax credit for each metric ton of qualified carbon oxide that is captured using carbon capture equipment and permanently stored. The credit rate, eligibility requirements, and facility standards were significantly enhanced by the Inflation Reduction Act of 2022, which also introduced the §6418 transfer mechanism that makes these credits accessible to third-party buyers.

The statute distinguishes between two broad categories of storage: geological storage (injecting CO₂ into underground formations) and qualifying utilization (converting captured carbon into a product that effectively sequesters it). Agricultural biochar systems are structured to satisfy the latter — specifically, the conversion of atmospheric CO₂ into a stable solid carbon compound that is incorporated into soil for long-term retention.

Understanding that positioning is the foundation for understanding what the generator's documentation is trying to prove.

How a Biological DAC System Works

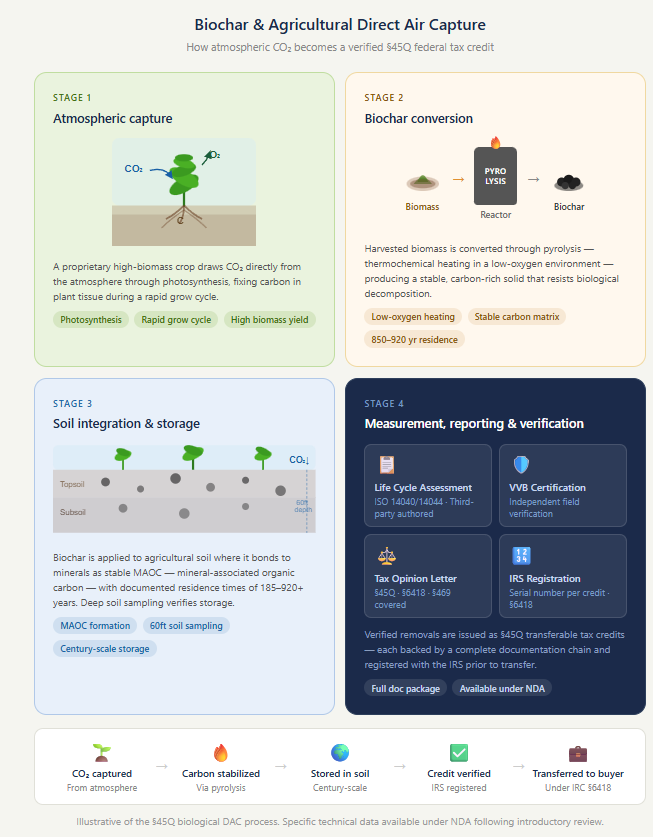

Conventional carbon capture — the kind associated with power plants and industrial facilities — intercepts CO₂ at the point of emission and compresses it for underground storage. Biological Direct Air Capture works differently. It uses living plants to pull CO₂ from ambient air through photosynthesis, then converts the captured carbon into a stable form through a thermal process called pyrolysis.

The three-stage pathway looks like this:

Stage 1 — Atmospheric capture. A high-biomass crop is cultivated specifically for its carbon uptake capacity. During its growth cycle, the plant draws CO₂ directly from the atmosphere and fixes it in plant tissue. Unlike forests, which accumulate carbon slowly over decades, high-yield agricultural crops can achieve meaningful carbon uptake within a single growing season. The crop functions as the capture equipment — it is the mechanism by which atmospheric carbon enters the system.

Stage 2 — Biochar conversion. After harvest, the biomass is processed through a pyrolysis reactor. Pyrolysis is a thermochemical process that heats organic material in a low-oxygen environment, preventing combustion. The result is biochar — a carbon-rich solid that retains the majority of the carbon originally fixed by the plant, now in a chemically stable form. The carbon that was atmospheric CO₂ weeks earlier is now locked in a solid matrix that resists biological decomposition.

Stage 3 — Soil integration and long-term storage. The biochar is returned to agricultural soil, where it integrates into the soil matrix and remains stable over timescales measured in centuries. Soil enhancement using microbial compost tea further supports carbon accumulation in the mineral-associated organic carbon (MAOC) fraction of the soil — the most stable and durable form of soil carbon storage. Deep soil sampling, GHG flux monitoring, and ongoing mass balance tracking document that the carbon remains sequestered.

The result is a closed-loop system: atmospheric CO₂ in, stable soil carbon out, with the conversion pathway documented at each stage.

Why Biochar Stability Is Central to §45Q Qualification

The permanence of storage is not incidental to §45Q — it is definitional. The statute requires secure, verifiable, long-term storage. For a geological storage system, permanence is demonstrated by the physical characteristics of the underground formation. For a biochar-based system, permanence is demonstrated through the chemistry of the biochar itself and the conditions of its soil integration.

Two scientific concepts are central here.

The first is the hydrogen-to-organic-carbon ratio (H:Corg). Biochar with a low H:Corg ratio has a more condensed aromatic structure, which makes it highly resistant to microbial decomposition. Laboratory screening of H:Corg ratios is the standard method for confirming that a given batch of biochar meets the stability threshold required for long-duration carbon credit accounting.

The second is mineral-associated organic carbon (MAOC). When biochar is integrated into soil alongside organic amendments, some of the carbon bonds chemically to soil minerals — a process that produces the most stable and persistent form of soil carbon. MAOC fractions have documented mean residence times measured in centuries, and the scientific literature supports their use as a basis for 100+ year crediting periods.

A credible §45Q generator working with a biochar system will have laboratory testing confirming H:Corg stability, annual soil sampling documenting MAOC accumulation, and an LCA that accounts for the system's full carbon balance — not just gross capture, but net storage after subtracting the operational footprint of running the facility.

What the Documentation Chain Should Look Like

When your client asks how you know the credit is real, the answer is the documentation chain. Here is what a well-structured biochar DAC generator should be able to produce, and what each document is actually demonstrating:

The Life Cycle Assessment establishes the net carbon performance of the system — gross atmospheric capture minus the emissions associated with operating the facility (energy inputs, equipment construction, transport, field application). The LCA should be authored by a credentialed third-party scientist following ISO 14040/14044 methodology, and it should report results at both the per-acre and program scale. This is the document that ties the physical operation to a verifiable metric-ton figure.

The VVB Certification (Validation and Verification Body) is the independent confirmation that the numbers in the LCA reflect what is actually happening in the field. The LCA is a model; the VVB certification is the audit of that model against observed operations. Both are necessary — neither alone is sufficient.

The Project Design Document describes the facility, the capture methodology, the monitoring protocols, and the placed-in-service timeline. For §45Q purposes, placed-in-service date documentation is a threshold requirement — the facility must have been placed in service within the statutory credit period, and that timing must be documentable.

The Tax Opinion connects the scientific and operational documentation to the legal standard. A properly scoped opinion will confirm that the storage methodology satisfies the §45Q(f) permanence requirement, that the generator is the appropriate credit claimant, and that the §6418 transfer is structured to be respected as a transfer of a tax attribute rather than an allocation.

The generator I represent has all four of these documents, prepared by independent third parties. They are available to qualified buyers following an introductory call and NDA.

The Question Your Client Will Ask

At some point in the diligence conversation, a CFO or sophisticated client will ask a version of this question: "How is burying charcoal in a field the same as storing carbon underground?"

The honest answer is that it isn't the same process — but it achieves the same statutory objective. Section 45Q is technology-neutral at its core. What it requires is capture of qualified carbon oxide, use of carbon capture equipment, and disposition through a process designed to achieve long-term storage. A biological system that removes CO₂ from the atmosphere, converts it into a chemically stable solid, and integrates that solid into soil where it will remain for centuries is designed to satisfy that standard — provided the documentation supports it.

The documentation is the answer to the question. If your client can review an ISO-compliant LCA showing verified net sequestration, a VVB certification confirming the field operations, laboratory data confirming biochar stability, and a tax opinion from a credentialed attorney concluding that the structure satisfies §45Q — that is a defensible factual record. The science is verifiable. The credit flows from the science.

If any of those elements are missing or can't be produced on request, that's the real answer to your client's question.

A Note on Your Role as Advisor

Understanding the science doesn't make you the expert on the science. Your role in a §45Q transfer transaction is the same as it is in any complex tax-advantaged investment: confirm that the documentation exists, that it's internally consistent, and that it's sufficient to support your client's tax position under examination.

You're not being asked to validate the LCA methodology or confirm that a particular H:Corg ratio meets the stability threshold. You're being asked to confirm that a credentialed third party has done that work, that their conclusions are documented, and that the documentation package holds together as a coherent record.

That's a manageable standard — and it's the right one.

This article is informational and does not constitute tax, legal, or accounting advice. Readers should conduct independent diligence and consult qualified advisors regarding their specific circumstances.